EXECUTIVE SUMMARY

- UN CHIEF CALLS FOR MAXIMUM RESTRAINT AFTER IRAN’S ATTACK ON ISRAEL - RTRS

- US WILL NOT TAKE PART IN ANY ISRAELI RETALIATORY ACTION AGAINST IRAN - RTRS

- METALS SPIKE ON LME AFTER RUSSIAN SUPPLY HIT BY US, UK SANCTIONS - BBG

- DALY SEES NO URGENCY FOR THE FED TO CUT RATES - MNI BRIEF

- ECB WILL CUT RATES JUN 6, BAR SURPRISES - VILLEROY - MNI BRIEF

- CHINA H2 COMMODITIES DEMAND TO SHOW MIXED SECTOR PERFORMANCE - MNI

- STIMULUS SEEN BOOSTING CHINA MANUFATCURING. OVERCAPACITY - MNI

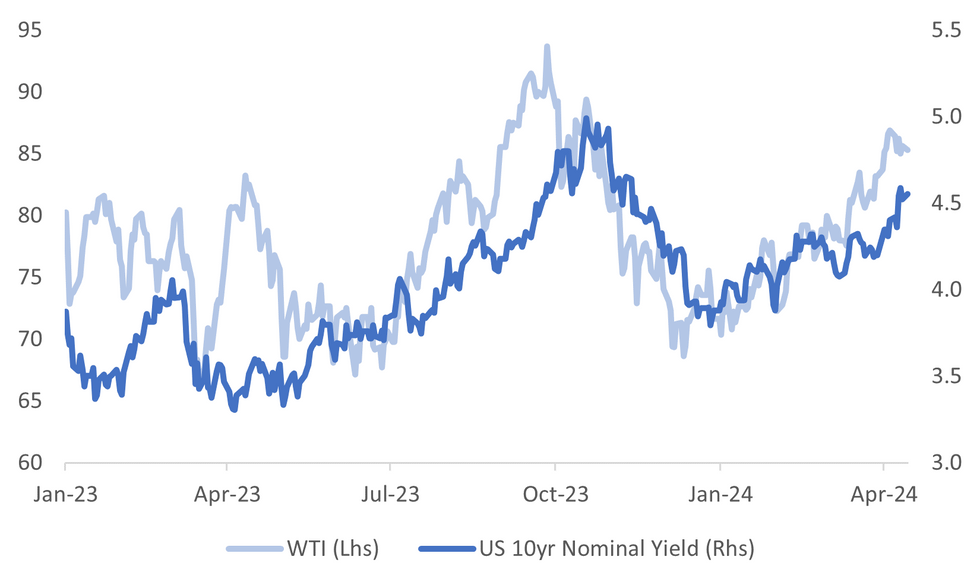

Fig. 1: WTI Versus US 10yr Nominal Tsy Yield

Source: MNI - Market News/Bloomberg

U.K.

POLITICS (BBG): Rishi Sunak is resisting advice from allies to set the date for the UK general election, which they say would help him to head off a threatened leadership challenge by Conservative Party rebels next month.

EUROPE

GERMANY/CHINA (BBG): German Chancellor Olaf Scholz will take a delicate message to China this week: Beijing has not acted on European warnings to end discriminatory business practices and failure to do so will result in an escalation in tensions.

ECB (MNI BRIEF): Bank of France Governor Francois Villeroy says the European Central Bank will cut rates at its Governing Council meeting on June 6, "barring any surprises".

POLITICS (POLITICO): Two months ahead of June’s Europe-wide election, Brussels is abuzz with European diplomats and officials warning that European Commission President Ursula von der Leyen is not a shoo-in for another five year term leading the EU’s executive.

UKRAINE (BBC): “Ukraine army chief says Russia making significant 'gains' in east of country”

The head of Ukraine's military has warned the battlefield situation in the east of the country has "significantly worsened" in recent days. Gen Oleksandr Syrskyi said Russia was benefitting from warm weather - making terrain more accessible to its tanks - and making tactical gains.

UKRAINE (POLITICO): Ukrainian President Volodymyr Zelenskyy said Iran's attack on Israel Saturday night is a "wake-up call" for Washington to get moving on supporting American allies.

UKRAINE (POLITICO): Germany agreed to send a Patriot air-defense system to Ukraine, Chancellor Olaf Scholz said on Saturday, but Berlin hasn't relented on its refusal to provide Kyiv with Taurus cruise missiles.

IRAN (POLITICO): French Foreign Minister Stéphane Séjourné on Sunday issued a statement recommending that French nationals living in Iran “temporarily leave the country.” The German Foreign Office has asked its citizens to do the same.

U.S.

US/CHINA (BBG): Treasury Secretary Janet Yellen said the US wouldn’t take “anything off the table” in response to China’s manufacturing capacity, including the possibility of additional tariffs to stem what she has described as a flood of cheap goods into the US market.

US/ISRAEL (RTRS): President Joe Biden warned Prime Minister Benjamin Netanyahu the U.S. will not take part in a counter-offensive against Iran, an option Netanyahu's war cabinet favors after a mass drone and missile attack on Israeli territory, according to officials.

FED (MNI BRIEF): San Francisco Federal Reserve President Mary Daly said Friday she's in no hurry to lower borrowing costs, citing a strong labor market and the "bumpy ride" across recent inflation data, adding to the list of officials showing more hesitancy this week following stronger-than-expected price gains.

FED (MNI BRIEF): Kansas City Federal Reserve President Jeff Schmid said Friday he'd prefer the central bank remain patient and wait for clear and convincing evidence that inflation is on track to hit the 2% target before adjusting the stance of policy, also suggesting he prefers the Fed not slow down on QT anytime soon.

OTHER

MIDDLE EAST (RTRS): United Nations Secretary-General Antonio Guterres on Sunday warned members not to further escalate tensions with reprisals against Iran, while the U.S. warned the Security Council it would work to hold Tehran accountable at the U.N. Guterres, speaking to a meeting of the U.N. Security Council, told member states that the U.N. charter bars the use of force against the territorial integrity or political independence of any state as he also condemned Iran's attack on Israel.

IRAN (RTRS): Turkish, Jordanian and Iraqi officials said on Sunday that Iran gave wide notice days before its drone and missile attack on Israel, but U.S. officials said Tehran did not warn Washington and that it was aiming to cause significant damage.

COMMODITIES (BBG): Aluminum and nickel surged on the London Metal Exchange as traders responded to new US and UK sanctions that banned deliveries of any Russian supplies produced after midnight on Friday. The new restrictions, aimed at curbing President Vladimir Putin’s ability to fund his military, inject major uncertainties into metals markets that have already been reshaped in the aftermath of Russia’s invasion of Ukraine.

CHINA

COMMODITIES (MNI): Chinese demand for steel and copper construction products will fall over the second half despite government support measures, while appetite for those commodities used in manufacturing will grow as industrial output strengthens, local researchers have told MNI.

MANUFACTURING (MNI): China’s manufacturing investment is set to maintain strong growth throughout the year thanks to policy stimulus, but weak demand means overcapacity will grow as well, depressing corporate profits and adding to the potential for trade friction, advisors and analysts told MNI.

EQUITIES (NATIONAL BUSINESS DAILY): last week published a key guideline for the high-quality development of China's capital market, National Business Daily reported. The last two guidelines published in 2004 and 2014 precipitated bull markets with the Shanghai Composite Index reaching 6,124 points in 2007 and 5,178 points in 2015.

PROPERTY (YICAI): Authorities must improve the “white list” of property projects eligible to receive financial support, according to He Lifeng, vice premier of the State Council, noting lenders need to optimise and speed up loan approval and issuance.

ECONOMY (SECURITIES TIMES): Chinese economists are upbeat on the policies the government rolled out in 1Q, especially initiatives related to stabilizing the capital market, the Securities Times reports, citing a survey it did.

ECONOMY (SHANGHAI SECURITIES NEWS): China’s economy has maintained the momentum of a sustained recovery as leading indicators including PMI show an expansion trend, according to the Shanghai Securities News.

POLICY (BBG): China withdrew cash from the banking system for a second consecutive month, signaling its caution toward monetary easing as currency depreciation pressures mount.

CHINA MARKETS

MNI: PBOC Conducts CNY100 Bln MLF Mon; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY100 billion via 1-year MLF and CNY2 billion via 7-day reverse repo on Monday, with the rates unchanged at 2.50% and 1.80%, respectively. There is CNY4 billion reverse repos matures today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:37 am local time from the close of 1.8336% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 44 on Friday, compared with the close of 48 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0979 on Monday, compared with 7.0967 set on Friday. The fixing was estimated at 7.2444 by Bloomberg survey today.

MARKET DATA

NZ FEB. NET MIGRATION ESTIMATE +7,630; PRIOR +3,950

NZ FEB. ANNUAL NET IMMIGRATION WAS 130,856

NZ BNZ MARCH SERVICES PSI FALLS TO 47.5; PRIOR 52.6

JAPAN FEB CORE MACHINERY ORDERS +7.7% M/M; EST. +0.8%; PRIOR -1.7%

JAPAN FEB CORE MACHINERY ORDERS -1.8% Y/Y; EST. -6.0%; PRIOR -10.9%

CHINA 1YR MLF 2.50%; MEDIAN 2.50%; PRIOR 2.50%

CHINA 1YR VOLUMES 100Bn YUAN: MEDIAN 170BN YUAN: PRIOR 387bn YUAN

MARKETS

US TSYS: Treasury Futures Erase Friday Moves As Geopol Tensions Simmer

- Treasury futures have continued their move lower, after briefly seeing some strength during the morning session. Jun 24' 10Y futures reached a post open high of 108-18+, before reversing those moves to trade at intraday lows of 108-08+, we trade just off those levels as Europe logs in down - 11+ at 108-10+.

- Earlier there was a 10Y block trade in 2.95k size at 108-14+, likely seller.

- Cash Treasury curve has bear-steepened, and erased earlier gains the 2Y yield +2.2bps at 4.918%, 10Y +3.1bp to 4.552%, while the 2y10y is +0.681 at 36.827

- Looking ahead: Retail Sales and Fed Speak with Dallas Fed Logan, NY Fed Williams Bbg TV interview, SF Fed Daly keynote remarks.

JGBS: Futures Stronger But At Session Lows, Light Local Calendar Again Tomorrow

JGB futures are stronger, +8 compared to settlement levels, but dealing at the bottom of today’s trading range.

- Outside of the previously outlined Machinery Orders, domestic drivers have been light on the ground. Accordingly, today’s price action has tracked fluctuations in US tsys in today’s Asia-Pac session.

- US tsys are dealing 3-4bps cheaper despite Iran’s military launching drones and missiles against Israel over the weekend, in a significant escalation of hostilities.

- Later today, the US data calendar includes Retail Sales and Fed Speak: Dallas Fed Logan, IMF/BoJ conf, Tokyo (no text, Q&A), NY Fed Williams Bbg TV interview, SF Fed Daly keynote remarks, Stanford (text, Q&A).

- Cash JGBs are dealing slightly mixed across the curve. The benchmark 10-year yield is 0.3bp higher at 0.858% versus the YTD high of 0.871%, set last week.

- The swaps curve has twist-steepened, with rate moves bounded by +/- 3bps. Swap spreads are mixed, but wider beyond the 10-year.

- Tomorrow, the local calendar is empty apart from an auction for Enhanced-Liquidity of 5-15.5-year JGBs.

AUSSIE BONDS: Slightly Richer, Tracking US Tsys, Local Calendar Light Until Jobs Data On Thursday

ACGBs (YM +3.0 & XM +2.5) are stronger but at or near session lows after US tsys open the week cheaper.- After closing 4-8bps richer across benchmarks last week, cash US tsys are dealing ~3bps cheaper in today’s Asia-Pac session. This comes despite Iran’s military launching drones and missiles against Israel over the weekend, in a significant escalation of hostilities.

- Cash ACGBs are 2-3bps richer, with the AU-US 10-year yield differential at -30bps. At -30bps, the cash differential currently sits at the bottom of the range of +/-30bps which has been observed since November 2022.

- A simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is 9bps too low versus its fair value.

- Swap rates are flat to 1bp lower.

- The bills strip is richer, with pricing +1 to +4.

- RBA-dated OIS pricing is slightly softer across meetings. A cumulative 22bps of easing is priced by year-end.

- The highlight of this week’s local calendar is the Employment Report for March on Thursday. The calendar is light until then.

NZGBS: Richer, Closed On Strong Note, Neutral OCR About 3.9% (RBNZ)

NZGBs closed on a strong note, with benchmark yields 7bps lower. While the local market opened stronger on the back of US tsys’ positive close on Friday, weak domestic data aided today’s strong close.

- As previously noted, the NZ Performance of Services Index fell to 47.5 in March from a revised 52.6 in February.

- Indeed, the local market strengthening through the session countered the ~2bps cheapening in US tsys during today’s Asia-Pac session.

- (Bloomberg) The RBNZ commented on neutral interest rates in an article on Monday. “Due to New Zealanders’ high inflation expectations, the OCR would currently need to be about 3.9% to neither tap the brakes nor push on the accelerator of the economy”. The OCR is 5.5% “which is therefore clearly contractionary”. (See link)

- Swap rates closed 5-6bps lower, with implied swap spreads wider.

- RBNZ dated OIS pricing closed flat to 2bps softer across meetings. A cumulative 39bps of easing is priced by year-end.

- The local calendar sees NZ REINZ House Sales tomorrow, ahead of Q1 CPI on Wednesday.

FOREX: Risk Currencies Outperform Yen, As Restraint Called For In Israel/Iran Conflict

The BBDXY sits little changed for Monday's session to date, last near 1259. This masks divergent trends within the G10 space though, with early yen and CHF gains giving way to a risk on feel for FX markets.

- USD/JPY has climbed to fresh cyclical highs, last at 153.80/85, around 0.40% weaker in yen terms versus end Friday levels in NY. Earlier lows were just under 153.00, as the market opened cautiously after the weekend Iranian missile/drone attacks on Israel.

- However, with the UN/G7 calling for restraint and US President Biden reportedly telling the Israeli leader the US would not participate in retaliatory attacks, has aided risk appetite as the session has progressed.

- Macro markets have reversed some of Friday's trends, with US equity futures up close to 0.30%, while US yields are higher across the benchmarks. USD/CHF is a touch higher, last near 0.9145.

- AUD is among the stronger G10 performers, up around 0.25%, last above 0.6480. Two other sources of support have been evident for the A$, with firmer China equities helping, along with a bounce in metal prices following US and UK sanctions on Russia.

- The Kiwi is mixed today, up only against the JPY, CHF and unchanged against the USD. NZD/USD was last near 0.5945. The RBNZ released a piece earlier where they suggest the OCR is "Contractionary" above the neutral cash rate of 3.9%, while NZ PSI saw its biggest contraction in two years falling from 53 to 47.5.

- Looking ahead, the Fed’s Logan and Williams appear and March retail sales and April Empire manufacturing are released. The ECB’s Lane and BoE’s Breeden speak, and euro area February IP is released.

ASIA EQUITIES: China Equities Outperform As Tighter Market Supervision Is Expected

Hong Kong and China equity markets are mixed today, with China mainland equities rallying. The move higher could be linked to China vowing to tighten stock market supervision after the rebound in equities has stalled, which was announced late Friday afternoon while the CSI300 have now broken back above the 20, 50 & 100-day EMA. Earlier the 1yr MLF was kept on hold at 2.50%.

- Hong Kong equities are lower today with HSTech down 0.88% after being down as much as 2.34% at one stage, Mainland Property Index is down 0.95%, the HSI is down 0.56%, the HS China Enterprise which tracks China owned companies is faring slightly better down just 0.23%. In China, equity markets are higher, with the CSI300 up about 2.10%, while the CSI1000 is down 0.53%

- China Northbound saw -7.4b of inflows on Friday, with the 5-day average at -2.29billion, while the 20-day average sits at 0.24billion yuan.

- (Bloomberg) China Vows to Tighten Stock Market Supervision as Rebound Stalls - (See link)

- In the property space, China Vanke is reassuring investors by outlining plans to address liquidity pressure and operational challenges, emphasizing the use of its own resources and existing financing facilities to stabilize operations and reduce debt. Despite recent stock and bond declines following credit rating downgrades, Vanke's executives deny rumors and controversies, affirming their commitment to timely project completion and normal overseas business activities, while facing pressures from China's real estate crisis and upcoming debt maturities.

- China's steel exports surged in March to the highest level since 2016, driven by weakened domestic demand amid the country's property crisis, prompting traders to seek more profitable markets. This trend underscores concerns raised by US Treasury Secretary Janet Yellen about Chinese overcapacity across emerging industries, with steel exports helping to offset declining domestic demand and affecting global steel markets.

- Efforts by the US to persuade the Netherlands and Japan to further restrict Chinese access to semiconductor technology faced resistance this week, as both countries sought more time to assess existing limits and awaited the outcome of the US presidential election. The impasse highlights the uncertainty surrounding President Joe Biden's reelection prospects and his administration's attempts to hinder China's technological advancement, particularly in light of potential policy shifts depending on the election outcome.

- Looking ahead, New Home Prices, GDP, Industrial Production & Retail Sales all expected tomorrow.

ASIA PAC EQUITIES: Equities Head Lower As Geopol Tensions Persist, EM Currencies Weaken

Regional Asian equities have pulled back on Monday as worries about potentially escalating tensions in the Middle East rattled financial markets, pushing investors to look for safer places for their money. U.S. futures rose and oil prices fell despite tensions roiling the Middle East where an attack late Saturday marked the first time Iran had ever launched a military assault on Israel. Regional Asian FX is lower, with TWD & KRW near multi-year lows. The economic data calendar is light on today with just Japan Machine Orders which surged in Feb, while New Zealand has PSI data which dropped below 50, to 47.5 in Mar and net migration jumped to 7,630 in Feb from a revised 3,650 in Jan.

- Japan equities equities are lower today tension in the middle east is seen as the major catalyst for the move. The yen has just broken the Friday lows and is now trading above 153.50, traders will be alert for yen intervention. Earlier Core Machine Orders were well above estimates coming in at 7.7% vs 0.8% expectation signifying a robust recovery and potential expansion in Japan's manufacturing and production sectors, positioning the country for further economic growth and development. The Topix is down 0.24%, while the Nikkei 225 is down 1.09%

- South Korean equities dropped as much as 1.5% in early morning trading and hit the lowest since March 7, erasing its year-to-date gain amid increased geopolitical risks after Iran launched an attack on Israel. The KRW has gapped lower this morning, after weakening on Friday with the currency now down 2.56% over the past 5 days. The Kospi has recovered majority of the earlier losses to trade down just 0.45%.

- Taiwan equities are lower today, there has been little in the way of local market headlines or economic data for the region with the next major data released not until Apr 22 when Unemployment and Export Orders are due out. Similar to the KRW, the TWD has weakened recently trading at 32.362 and now eyes multi year lows at 32.50. The Taiex has continued to trade off throughout the session and now down 1.02%

- Australian equities are lower today following global markets lower as risk assets track lower. Mining stocks have bucked the trend as commodity prices rise. The ASX200 is down 0.42%

- Elsewhere in SEA, New Zealand Equities are down 0.45%, Singapore equities are down 1.08%, Malaysian equities are 0.42% lower, while Philippines equities continue their drop down another 1.24% and now off 5.60% from recent highs made Apr 2nd.

OIL: Crude Eases As Markets Don’t Expect An Escalation In The Middle East

After a short-lived spike at the start of the session, oil prices are moderately lower today as fears of an escalation in the Middle East fade and a risk premium is also priced in. Energy markets are likely to continue to watch development closely though. WTI is down 0.3% to $85.45/bbl after a low of $84.88, and Brent -0.2% to $90.30 after falling briefly below $90 earlier to a low of $89.77. The USD index is slightly lower.

- Iran said it has achieved its objective and also doesn’t want an escalation particularly with the US. The US has apparently warned Israel privately not to retaliate but war cabinet minister Gantz has said that it will “exact a price” when the time is right.

- Shipping risks in the Middle East have risen with Iran seizing an Israeli cargo vessel in the Strait of Hormuz. The closure of the Strait is a key concern.

- Geopolitical risks in the Middle East and Russia, key oil-producing regions, plus signs of increased demand in the US and China in addition to OPEC’s continued output cuts are driving consideration that crude will reach $100/bbl. Any second round effects from higher energy prices will be monitored closely by central banks.

- Later the Fed’s Logan and Williams appear and March retail sales and April Empire manufacturing are released. The ECB’s Lane and BoE’s Breeden speak, and euro area February IP is released.

GOLD: Higher After Friday’s Spike Reversal

Gold is 0.6% higher at $2357.66 in the Asia-Pac session, after Iran’s military launched drones and missiles against Israel over the weekend, in a significant escalation of hostilities.

- Interestingly, US tsys aree dealing weaker today after Friday’s rally.

- Today’s move comes after bullion surged to a fresh record high of $2431.52 on Friday before the gains were pared.

- The underlying safe-haven demand for the US dollar exerted itself in the latter half of Friday’s session, prompting a significant reversal lower for the precious metal.

- (Bloomberg) Gold is in an “unshakeable bull market,” according to Goldman Sachs Group Inc., which raised its year-end forecast for the precious metal to $2,700/oz. (See link)

- According to MNI’s technicals team, the next objective is $2376.5, a Fibonacci projection.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/04/2024 | 0630/0230 |  | US | Dallas Fed's Lorie Logan | |

| 15/04/2024 | 0900/1100 | ** |  | EU | Industrial Production |

| 15/04/2024 | 1115/1215 |  | UK | BoEs Breeden on Payments Innovation | |

| 15/04/2024 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 15/04/2024 | 1230/0830 | ** | | CA | Wholesale Trade |

| 15/04/2024 | 1230/0830 | *** | | US | Retail Sales |

| 15/04/2024 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/04/2024 | 1400/1000 | * | | US | Business Inventories |

| 15/04/2024 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 15/04/2024 | 1415/1615 | | EU | ECB's Lagarde Speaks On ECB Podcast | |

| 15/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 15/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |